Heavy! "cut interest rates"

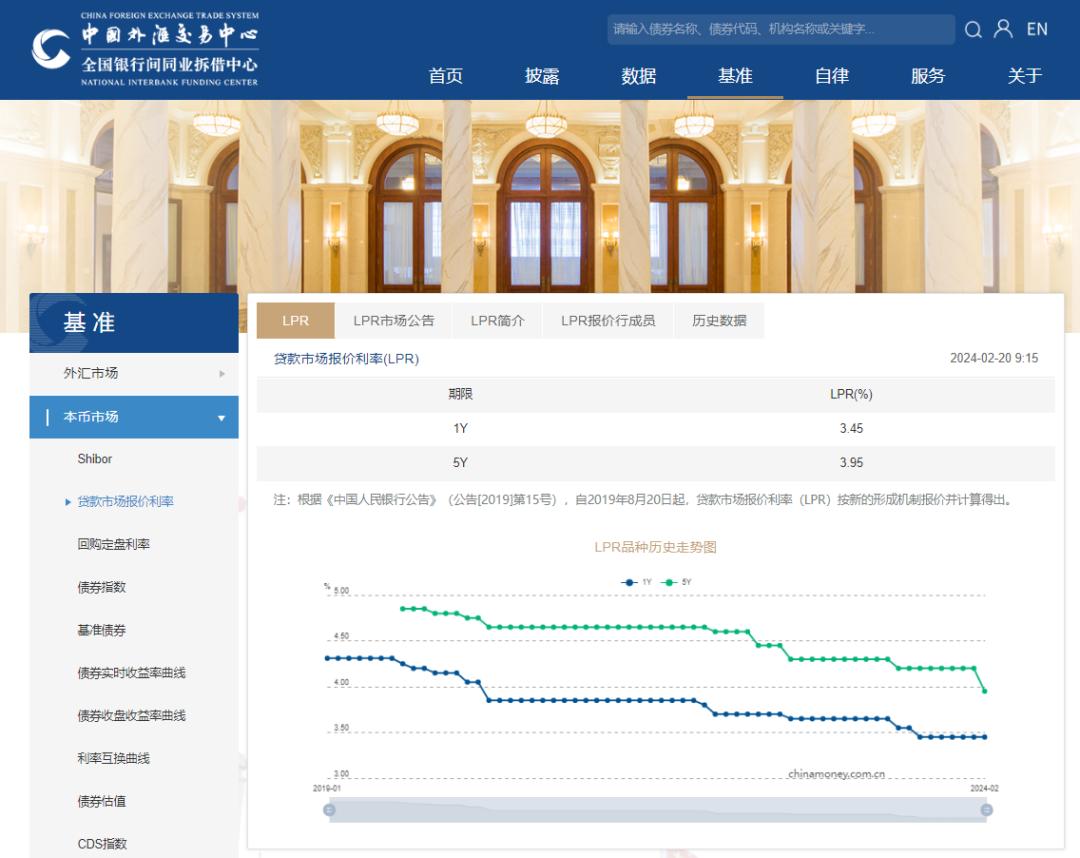

The quoted interest rate (LPR) in the loan market ushered in the first downward adjustment in 2024, and the varieties with a term of more than five years dropped by 25 basis points, while the varieties with a term of one year remained unchanged. Industry analysts believe that the downward trend of LPR will further drive down the real loan interest rate and promote the steady decline of social financing costs. Since August 20, 2019, the quoted interest rate (LPR) of the loan market has been quoted and calculated according to the new formation mechanism. According to the historical trend chart of LPR varieties released by China Foreign Exchange Trading Center, 25 basis points is the largest decline of 5-year LPR since August 2019.

According to the news of WeChat WeChat official account "People’s Bank of China" on February 20th, the People’s Bank of China authorized the National Interbank Funding Center to announce that on February 20th, 2024, the loan market quoted interest rate (LPR) was 3.45% for one year and 3.95% for five years or more. The above LPR is valid until the next LPR release.

Previously, on January 22nd, the People’s Bank of China authorized the National Interbank Funding Center to announce that the quoted interest rate (LPR) of the loan market on January 22nd, 2024 was 3.45% for one year and 4.2% for five years or more.

Compared with the LPR published in January, the one-year LPR remained unchanged in February, and the LPR over five years was lowered by 25 basis points.

Historical trend chart of LPR varieties

Double "asymmetric" decline

Previously, on February 18th, the People’s Bank of China launched a 105 billion yuan open market reverse repurchase operation and a 500 billion yuan medium-term lending facility (MLF) operation. The 7-day reverse repurchase rate and the 1-year MLF rate were 1.80% and 2.50% respectively, which remained unchanged from the previous period. Analysts had previously predicted that the LPR would be lowered under the background that the operating interest rate of MLF remained unchanged, and the decline of LPR over five years was greater than that of LPR over one year.

Why is there "asymmetry" between MLF and LPR?

Everbright said that LPR is formed by adding points based on MLF interest rate, and the range of adding points mainly depends on the quotation bank’s own capital cost, market supply and demand, risk premium and other factors.

National business daily, citing the analysis of insiders, thinks that the relationship between LPR and MLF interest rate should be further diluted in the future. Compared with MLF interest rate, whether the financing cost of real economic entities can be reduced is more important for economic growth, and the actual indication of LPR in this respect is stronger.

"LPR has become the main reference benchmark for loan interest rate pricing." Ming Ming, chief economist of CITIC Securities, said that LPR is formed by quotations from 20 commercial banks, and there are open rules for the selection of quotation banks, the quotation time and the final published calculation method, which are quoted once a month on the 20th. When quoting, quotation banks will adjust their quotations according to their own capital costs, market supply and demand, risk premium and other factors. The market generally believes that LPR, as the benchmark of bank loan pricing, is directly related to the changes of financing costs and financial expenditures of enterprises and residents, and business entities pay more attention to LPR and reflect it more sensitively. The downward trend of LPR will also help to further reduce the actual loan interest rate and promote the steady decline of social financing costs.

At the same time, whether LPR can decline depends on whether the bank’s capital cost can go down, and the deposit cost is an important factor affecting the bank’s capital cost. Major banks have cut deposit interest rates four times since 2022, which will further open up the space for LPR to go down and banks to make profits.

Everbright fixed income also said that in recent days, the bank’s capital cost has fallen by a large margin, which will help promote the downward trend of LPR. On the one hand, in September and December last year, major banks actively lowered the deposit interest rate according to their own business needs and market supply and demand. On the other hand, since January 25th this year, the interest rates of refinancing and rediscounting for supporting agriculture and supporting small enterprises have been lowered by 0.25% respectively, and the deposit reserve ratio of financial institutions has been lowered by 0.5% since February 5th this year. On the other hand, the cost of issuing active debt instruments of banks has also dropped significantly. On February 9th, the interest rates of 1Y AAA CD and 5Y commercial bank bonds were lower than those of 33bp and 30bp at the end of November last year, respectively.

Everbright Finance pointed out that in retrospect, the MLF-LPR linkage mechanism does not mean that the two need to be adjusted equally. MLF "stays put" and LPR is lowered separately. In September 2019, December 2021 and May 2022, the MLF interest rate remained unchanged for three times, while the LPR spread was lowered. Among them, in September 2019 and December 2021, the 1Y-LPR was lowered by 5bp alone, and in May 2022, the 5Y-LPR was lowered by 15bp alone.

Observing the commonness of the above three LPR quotation adjustments, it is found that the liquidity environment is relatively loose during the period, and there are "wide currency" operations such as RRR reduction in the month or in the early stage, which pushes down the capital cost of the bank’s debt side, thus providing operational space for LPR downward adjustment. This time, the MLF maintained a "price level", mainly considering the RMB exchange rate constraint.

Dongfang Jincheng also pointed out that the MLF operating interest rate continued to "stay put" in February, which may be related to factors such as the RRR cut in the month and the expected downward adjustment of LPR quotation. In addition, in November and December, 2023, major domestic banks lowered the deposit interest rate, which helped to push down the LPR quotation and replaced the MLF interest rate reduction to some extent.

Another "asymmetry" is the 1-year and 5-year LPR. The last asymmetric decline of LPR was in August 2023. At that time, the one-year period declined, while the five-year period remained unchanged.

Compared with the data in September 2019, before this downward adjustment, the 5-year LPR was only lowered by 65 basis points, which was lower than the cumulative decline of 75 basis points in the 1-year LPR, so there is room for unilateral downward adjustment in the 5-year period.

China securities journal believes that another reason is that asymmetric interest rate cuts may be more in line with the demands of stable real estate and stable economy. "LPR over five years is the pricing benchmark of individual housing loans. The decline of LPR over five years will further reduce the interest expenses of residential mortgages and promote the stable development of the real estate market." Dong Ximiao, chief researcher of Zhaolian, said.

When will the mortgage drop?

According to national business daily, according to the requirements of the relevant announcement issued by the central bank, financial institutions should negotiate with customers of floating interest rate loans from March 1, 2020, and choose one of two interest rate pricing methods: fixed interest rate or floating interest rate, that is, LPR+ plus points (the points can be negative). Under normal circumstances, a fixed interest rate is chosen, and the annual repayment rate remains unchanged until all loans are paid off; However, if the floating interest rate is selected, the mortgage interest rate will be priced by LPR as the pricing benchmark+basis point (1 basis point is 0.01%).

It should be noted that after the LPR adjustment, the user’s mortgage interest rate is not adjusted immediately. Generally speaking, the repricing date of mortgage interest rate is January 1st of each year or the loan issuing date (different banks have different policies, so users can choose when signing loan agreements). Therefore, for the existing mortgage, the new interest rate will be obtained according to the latest LPR quoted interest rate and the basis point agreed in the contract on the interest rate repricing date, and will be implemented in the next cycle.

Source | Observer Network

Keep sliding to see the next one.

Heavy! "cut interest rates" on Observer. com.

Observer likes to share. Read and write a message. Slide up to see the next one.

Original title: "Heavy! "cut interest rates" "

Read the original text